14.0%OFF

14.0%OFF

Download App

| >> | LShop | >> | Book | >> | Economics, Finance, ... | >> | Finance & Accounting | >> | Handbook Of Modeling... |

14.0%OFF

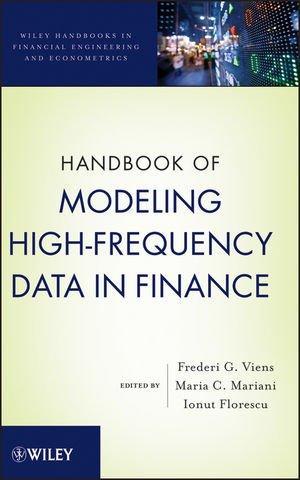

Handbook of Modeling High-Frequency Data in Finance (Wiley Handbooks in Financial Engineering and Econometrics)

-

ISBN

:

9780470876886

-

Publisher

:

Wiley

-

Subject

:

Finance & Accounting, Economics

-

Binding

:

HARDCOVER

-

Pages

:

456

-

Year

:

2011

₹

15183.0

14.0% OFF

14.0% OFF

₹

13057.0

13057.0

13057.0

Buy Now

Shipping charges are applicable for books below Rs. 101.0

View Details(Imported Edition) Estimated Shipping Time : 15-18 Business Days

View Details

-

Description

CUTTING-EDGE DEVELOPMENTS IN HIGH-FREQUENCY FINANCIAL ECONOMETRICSIn recent years, the availability of high-frequency data and advances in computing have allowed financial practitioners to design systems that can handle and analyze this information. Handbook of Modeling High-Frequency Data in Finance addresses the many theoretical and practical questions raised by the nature and intrinsic properties of this data.A one-stop compilation of empirical and analytical research, this handbook explores data sampled with high-frequency finance in financial engineering, statistics, and the modern financial business arena. Every chapter uses real-world examples to present new, original, and relevant topics that relate to newly evolving discoveries in high-frequency finance, such as:Designing new methodology to discover elasticity and plasticity of price evolutionConstructing microstructure simulation modelsCalculation of option prices in the presence of jumps and transaction costsUsing boosting for financial analysis and tradingThe handbook motivates practitioners to apply high-frequency finance to real-world situations by including exclusive topics such as risk measurement and management, UHF data, microstructure, dynamic multi-period optimization, mortgage data models, hybrid Monte Carlo, retirement, trading systems and forecasting, pricing, and boosting. The diverse topics and viewpoints presented in each chapter ensure that readers are supplied with a wide treatment of practical methods.Handbook of Modeling High-Frequency Data in Finance is an essential reference for academics and practitioners in finance, business, and econometrics who work with high-frequency data in their everyday work. It also serves as a supplement for risk management and high-frequency finance courses at the upper-undergraduate and graduate levels.

-

Author Biography

Frederi G. Viens, PhD, is Director and Coordinator of the Computational Finance Program at PurdueUniversity, where he also serves as Professor of Statistics and Mathematics. He has published extensively in the areas of mathematical finance, probability theory, and stochastic processes. Dr. Viens is co-organizer of the annual Conference on Modeling High-Frequency Data in Finance.Maria C. Mariani, PhD, is Pro-fessor and Chair in the Department of Mathematical Sciences at The University of Texas at El Paso. She currently focuses her research on mathematical finance, applied mathematics, and numerical methods. Dr. Mariani is co-organizer of the annual Conference on Modeling High-Frequency Data in Finance.Ionut Florescu, PhD, is Assistant Professor of Mathematics at Stevens Institute of Technology. He has published in research areas including stochastic volatility, stochastic partial differential equations, Monte Carlo methods, and numerical methods for stochastic processes. Dr. Florescu is lead organizer of the annual Conference on Modeling High-Frequency Data in Finance.

Related Items

-

of

-

OFFER

Derivatives Simplified: An Introduction to Risk Management

P. Bhaskar

Starts At

376.0

376.0

495.0

24% OFF

-

OFFER

Multinational Corporate Finance: Associateship Study Manual (Bankers Workbook)

Mark Largan

Starts At

5820.0

7973.0

27% OFF

-

OFFER

The Snowball: Warren Buffett and the Business of Life

A. Schroeder

Starts At

497.0

599.0

17% OFF

-

OFFER

More Money Than God: Hedge Funds and the Making of the New Elite

Sebastian Mallaby

Starts At

449.0

599.0

25% OFF

-

OFFER

Bank 2.0: How Customer Behavior and Technology Will Change the Future of Financial Services

Brett King

Starts At

4258.0

4436.0

4% OFF

-

OFFER

The Weekend That Changed Wall Street: An Eyewitness Account

Maria Bartiromo

Starts At

1977.0

2299.0

14% OFF